Get The Knowledge, Be In The Know

Want to know the fastest way to achieve your dream home, your ideal lifestyle, or the success you’ve been seeking? I’ll guide you every week.

I’m offering an exclusive look into the mindset and strategies of successful entrepreneurs and billionaires—how they’ve navigated the journey to success and what you can learn from them. It’s all about gaining the knowledge and mentorship you need to thrive.

That’s why I created this newsletter. It’s not just about business; it’s about unlocking the keys to success in every aspect of life—acquiring knowledge, building the right habits, and shaping the future you’ve envisioned.

From insights into entrepreneurial success to actionable advice on achieving your goals, this newsletter is your ultimate resource. Together, we’ll stay in the know and gain the knowledge that transforms aspirations into reality.

Ready to take the first step? Subscribe now and let’s thrive together.

✺ CATCH the LATEST VIDEO ✺

Water: How Much Should CEOs Drink Every Day?

Danijella Dragas: With a multitude of stressors, every executive at The Lending Corporation knows the challenges of maintaining balance and well-being in a demanding role. To help you prioritize health, The Lending Corporation has focused on bringing the renowned Mayo Clinic’s recommendations to the forefront, emphasizing some of the most crucial—and often overlooked—aspects of maintaining good health as a corporate leader.

The housing market in 2025 is expected to see a mix of modest improvements and lingering challenges, according to Fannie Mae’s Economic and Strategic Research Group. Economists predict the 30-year fixed mortgage rate will fluctuate throughout the year before stabilizing slightly above 6%.

The U.S. housing market in 2024 will be remembered as the slowest in over 30 years. The challenges began in 2022, when real estate transactions plummeted due to soaring mortgage rates and a persistent shortage of affordable housing inventory.

✺ CATCH the LATEST ✺

-

Mortgage Rates Are Quietly Shifting — Here’s What That Means

Mortgage rates are hovering at some of the lowest levels we’ve seen in years. At the same time, refinance activity is accelerating. Last week alone, refinances accounted for 57.4% of all mortgage applications — and that number continues to climb. This isn’t random movement. It’s positioning.

-

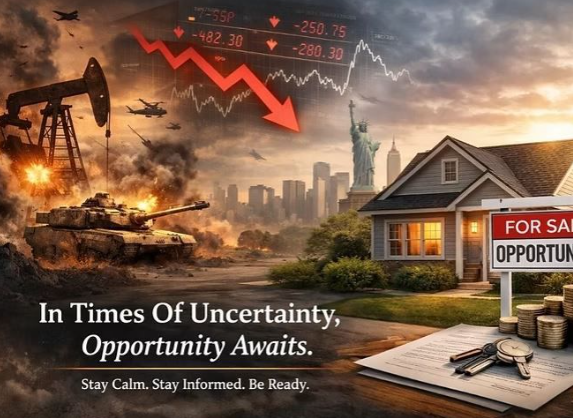

Global Conflict, Economic Uncertainty, and the U.S. Housing Market & Why Fear Often Signals Opportunity

How global conflict impacts the U.S. housing market. Global conflict affects housing through several key channel. Oil prices and inflation pressure: War and geopolitical instability, particularly in energy-producing regions, often disrupt oil supply. When oil prices rise, transportation, construction materials, and everyday living costs increase.

-

Why Mortgage Rates Went Up After the Fed Cut Rates

The Fed Doesn’t Directly Control Mortgage Rates

One of the biggest misconceptions is that the Federal Reserve directly sets mortgage rates. That’s not the case. The Fed sets short-term interest rates—the rate banks charge each other for overnight lending. Mortgage rates, however, are tied more closely to long-term bond markets, particularly the 10-year U.S. Treasury yield. When investors demand higher returns on those bonds, mortgage rates rise as well.

-

Federal Layoffs Add New Uncertainty to the Mortgage Market

Federal staffing cuts are once again making waves across the real estate and lending landscape. As the government shutdown continues, new rounds of reductions in force (RIFs) are raising concerns for lenders and borrowers who rely on federally backed mortgage programs.

-

Market Update

The Fed’s first 2025 cut lowers the target range to 4.00–4.25%. Projections suggest two more cuts this year, potentially bringing rates down to 3.50–3.75%. This marks another turn in the decades-long interest rate cycle, from the Volcker-era highs of 19% to the near-zero rates of the financial crisis and pandemic.

-

Housing Heat Check: Rates, Millennials & Builder Confidence Driving 2026

Mortgage rates continue to shape the outlook across housing and lending sectors, and the latest updates point to growing optimism. Builder confidence is holding steady while future sales expectations are rising.

-

Trump pick plants flag as Fed moves on rates

While the Fed voted to reduce interest rates by a quarter point, as expected, Stephen Miran was the only member of the 12-person panel to call for a half-point drop, which would have been a much more significant move for the Fed to take in one swoop.

-

Preparing for Closing: A Step-by-Step Guide

Closing on a loan is an exciting milestone—but it can also feel overwhelming without the right preparation. To make sure everything goes smoothly, it’s important to understand what happens once you receive the final approval or Clear to Close (CTC).

-

URGENT MARKET UPDATE – FED RATE CUTS COMING!

The Federal Reserve is projected to cut interest rates up to 5 times over the next year. This shift could quickly turn today’s buyer-friendly market into a fast-paced sellers’ market.

-

Ready to Stop Renting? Let’s Get You Home

Credit score not perfect? No problem. FHA loans offer flexible credit requirements and down payments as low as 3.5%. 2024 Avg. Rate: 5.25% for 30-year fixed. For our military heroes and veterans: no down payment required. Seriously—$0 down!

-

Major Step Toward Ending Mortgage Trigger Leads

When you apply for a mortgage, credit bureaus can sell your inquiry data to competing lenders—resulting in a flood of unsolicited calls, texts, and emails. This practice not only confuses homebuyers but also erodes your trust in the mortgage process.

-

The Bond Market Rally Has Begun!

The bond market has been waiting for this moment: tame or non-trending inflation. As a result, we’re seeing the first significant rally in quite some time, and here’s what it means for you: LOWER RATES.

-

Real Estate Industry Update

The U.S. housing market in 2024 will be remembered as the slowest in over 30 years. The challenges began in 2022, when real estate transactions plummeted due to soaring mortgage rates and a persistent shortage of affordable housing inventory. These issues persisted into 2023, further stalling the market.

-

Schedule Your Annual Check-Up!

As part of our commitment to your financial well-being, we’re excited to offer you our Identity Theft Annual Check-Up. This comprehensive review is designed to help you protect your identity, monitor your credit, and ensure peace of mind.

-

Here’s what Fannie Mae’s economists expect for 2025

The housing market in 2025 is expected to see a mix of modest improvements and lingering challenges, according to Fannie Mae’s Economic and Strategic Research Group.

-

Reverse Mortgage

Although many people spend decades planning for retirement, the topic often causes anxiety. In fact, a study by the National Institute on Retirement Security found that 56% of Americans are concerned about achieving a financially secure retirement.

-

Understanding Home Equity and Reverse Mortgage Eligibility

General knowledge says that borrowers need “substantial equity” in their homes to take a reverse mortgage. Obviously, if you own your home outright, that counts as substantial equity. But how much equity will be sufficient for borrowers with an existing mortgage? Here’s a look at equity in reverse mortgages.

-

Empower Your Success Beyond Numbers: One Decision at a Time

We want to bring your attention to an important new regulation that could affect your business: The Corporate Transparency Act (CTA). Passed by Congress, this law is designed to combat money laundering and terrorist financing, but it requires action from most corporations, LLCs, and similar entities doing business in the U.S.

-

$9 billion in potential HomeSafe Second loans

Our partners have already found $9 billion in potential HomeSafe Second loans that may help clients give the gift of a living inheritance and so much more. We can help you scan your database for those leads right now — with no identifying client information required.

-

Credit tips, plus my top credit cards

How many credit cards should you have? This is a question I often get asked. Like many things, it's personal, but I firmly believe if you have good credit, know how to use credit and are not going to go into debt, then around five credit cards would be reasonable.

-

How To Use Life Insurance To Protect Your Real Estate Holdings

Insurance can be a powerful tool for protecting real estate investments. Depending on their risk tolerance and skill set, real estate investors have different strategies for utilizing insurance and transferring risk. This may include increasing riders or coverage to providing extra coverages for such things as loss of rents, disabilities, private collections, additions or use.

-

What Are Conventional Loan Requirements?

Conventional loan requirements are pretty stringent—especially when compared to government-backed mortgages. Private lenders want to make sure that you can afford the property that you are buying and that you will repay the loan.